WuBlockchain is authorized by the author to translate and publish

This article provides statistical data on BNB Launchpad performance from 2021 to the present. It evaluates the current profitability level of Launchpad compared to historical data and calculates the long-term returns of holding BNB for IEO, benchmarking against ETH staking rewards. The goal is to provide a comprehensive analysis of “BNB returns.”

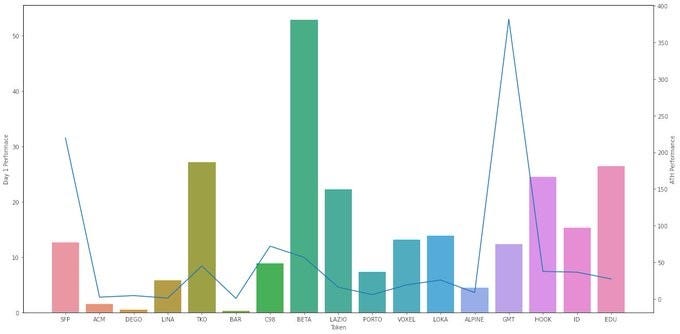

The graph above shows the historical data of Launchpad with the following indicators:

● D1 Gain: The price difference between the initial listing and the initial decentralized offering (IDO) in the first UTC+0:00.

● ATH Gain: The highest price compared to the IDO.

● BNB-based D1 ROI: The amount of BNB received by selling tokens acquired by investing 1 BNB on the first day.

● BNB-based ATH ROI: The amount of BNB received by selling tokens acquired by investing 1 BNB at the historical peak price.

Evaluation of profitability

Taking the median of all Launchpad projects since 2021, the median D1 Gain is 12.6x, ATH Gain is 25.7x, the BNB-based D1 ROI is 0.015, and the BNB-based ATH ROI is 0.031.

Regarding the three tokens launched since HOOK, all indicators are at an above-average level. The median D1 Gain of 24.4x is 1.9x the historical median, ATH Gain is 1.4x the historical median, the BNB-based D1 ROI is 1.5x, and the BNB-based ATH ROI is 1.3x. In other words, these projects during the bear market are actually more profitable than most projects during the bull market.

The current policies are also relatively friendly to arbitrage users. Compared to the inconsistent returns in the past, the BNB-based ROI of the three recent projects are around 2%. If the future Launchpad terms remain similar to these projects, users who engage in spot trading, shorting contracts through Venus, and participating in IEO can expect a relatively stable return.

Why is there feedback that it’s “less exciting”?

The reason is likely due to the lack of major breakthroughs. Products like SFP and GMT in 2021/2022 provided returns of hundreds of times, and holding onto them would yield significant profits. The time between the previous SFP and GMT was about one year, but after GMT, a year has passed without the emergence of projects with similar growth rates.

It’s normal for an outstanding project to leave a stronger impression compared to three above-average projects. When you look at the chart below, the first thing that comes to mind is finding GMT. The so-called BNB-based ATH ROI of 0.46 for GMT means that by investing 1 BNB, you could sell it at the peak for 0.46 BNB. SFP, on the other hand, could yield 1.56 BNB from 1 BNB invested! It’s no wonder people have a lasting impression. In comparison, the current maximum return of 0.0X is somewhat underwhelming.

However, it’s interesting to note that both SFP and GMT had relatively average D1 Gain, only 12x, which is half of the Hook/EDU projects. These three new projects have not been online for long and are operating in a bear market environment, where Ponzi-like patterns are less likely to thrive. Therefore, there should not be excessively high expectations for now.

Long-term returns of holding BNB

The annualized return of BNB Launchpad can be compared to ETH staking rewards. Over the past two and a half years, if tokens acquired on the first day were sold, the total BNB-based ROI would be 36%, with an annualized return of 14%. This appears slightly higher than the returns from ETH staking during the same period.

However, there are also the earnings from BNB Launchpool to consider. If we include the earnings from staking and withdrawing in the Launchpool, the total BNB-based ROI would be 52%, with an annualized return of 21%. This is nearly double the returns from ETH staking during the same period.

In the past year since the bear market, the overall project returns have been approximately 9.5%. Comparatively, the ETH staking APR benefiting from MEV income after the merge is around 6%. Therefore, even in a bear market, the BNB IEO returns have maintained a rate 1.5x higher than ETH staking.

If a bull market arrives, ETH staking returns are expected to benefit from MEV income, while BNB Launchpad may experience both quantity and price increases. However, the current ETH staking rate is relatively low compared to other Layer 1 solutions, indicating potential for a 2–3x increase in staking. This may dilute the returns due to increased staking activity. The capital invested in IEO has been relatively stable around 10 million, and with the allure of “ATH ROI,” BNB is relatively resilient in a bull market.

Additionally, both BNB and ETH are experiencing deflationary mechanisms through token burning, with BNB’s burning rate significantly faster. However, the returns from burning should directly reflect in the token price. BNB/ETH has historically shown an upward trend, and since 2021, BNB/ETH has mostly been fluctuating sideways. Therefore, comparing the returns from staking and Launchpad with those from ETH is reasonably justified.

Summary

Since the bear market, the overall comprehensive ROI of the three Launchpad projects have been in the upper-middle range of historical data, with indicators approximately 1.3~1.9x higher than the historical median. The stable BNB-based D1 ROI of around 2% makes it suitable for arbitrage.

It has been a year since projects like SFP and GMT that achieved phenomenal returns, allowing for a maximum return of up to 1.5x the initial investment of 1 BNB. The market feedback may be more negative due to the absence of such projects.

Comparing it to ETH staking, the long-term returns from holding BNB for IEO approximately 9.5%, which is 1.5x higher than ETH returns. During the previous bull market, BNB’s returns were approximately twice as high as ETH’s, and it is expected to be more resilient in future bull markets.

However, this analysis is based on a single dimension. In the next bull market, the use cases of ETH and BNB could be the key factors determining their returns. Currently, ETH Layer 2 development is progressing well, and it is crucial to observe whether BNB Chain can continue its momentum.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish